Nigeria’s fintech story over the last decade is genuinely impressive. From a cash-first economy to one where millions of people send money instantly from their phones. From manual bank transfers that took days to NIP transactions that clear in seconds. From a handful of licensed banks to hundreds of fintechs, neobanks, and payment processors.

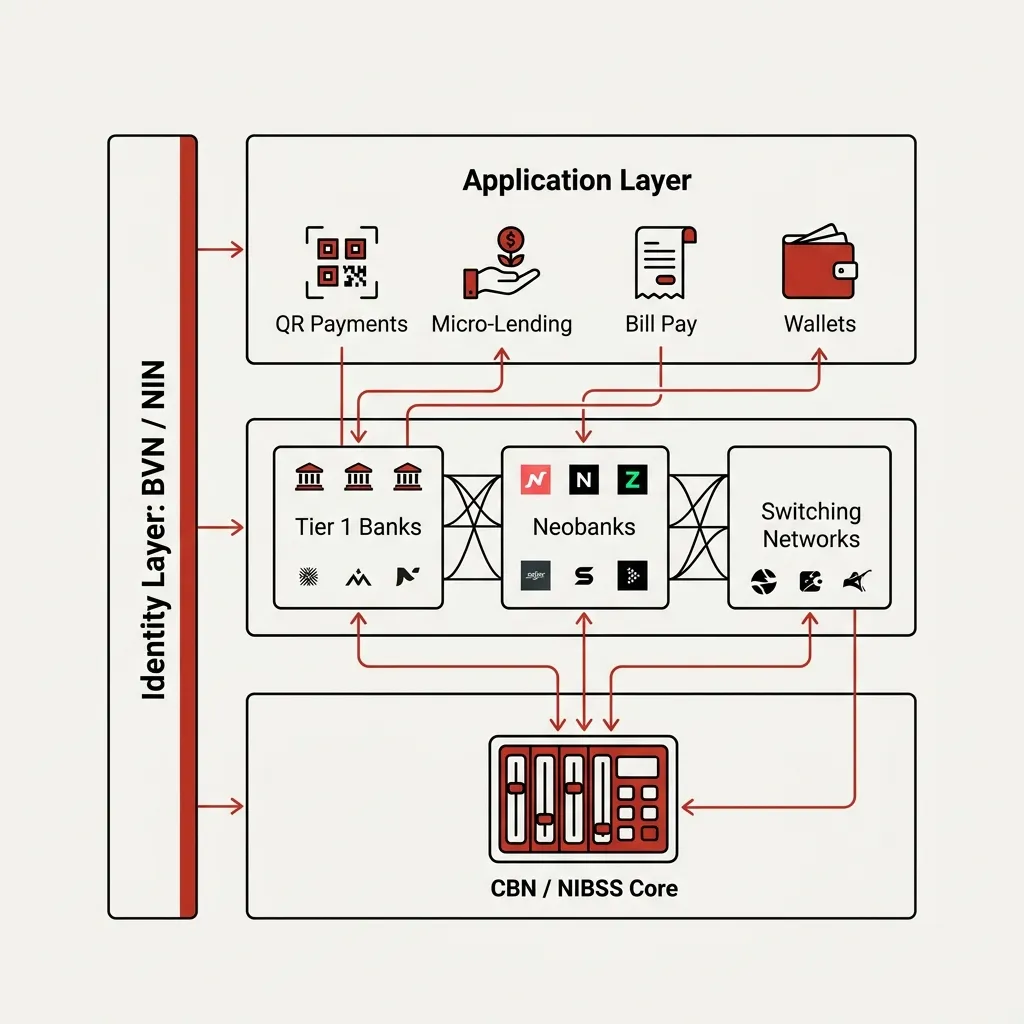

The rails that enable this — the NIP infrastructure, the BVN identity system, the CBN’s licensing framework — are real achievements. They made the last decade of growth possible.

But the next phase of growth is different. Embedded finance. Programmatic credit. Enterprise-grade payment infrastructure. Multi-currency operations. These demand something the ecosystem hasn’t fully built yet: reliable infrastructure designed for developers and businesses, not just consumers.

What the Current Infrastructure Does Well

It’s worth being precise about where Nigeria’s fintech rails are genuinely strong.

Real-time retail transfers work. NIP, operated by NIBSS, processes millions of transactions daily with sub-10-second settlement in most cases. For peer-to-peer and small-business payment flows, this is world-class.

Identity infrastructure is in place. BVN provides a national financial identity layer that most of the ecosystem can build on. NIN integration has extended this further. The ability to verify identity programmatically at account opening removes a friction point that cripples fintech in markets without equivalent systems.

The licensing framework has matured. The distinction between Payment Service Banks, Mobile Money Operators, Payment Solution Service Providers, and full commercial banks gives the ecosystem room to innovate without requiring every company to build a full bank. The tiered structure works.

Incumbents have opened APIs. The major banks now offer API access — some through direct integration, others through aggregators like Mono, Stitch, and Okra. The shift from “call the bank’s enterprise team” to “generate an API key” has happened.

Where the Infrastructure Falls Short

The gaps are not random. They cluster around the requirements of more sophisticated financial products.

Reliability at the Application Layer

The NIP rails themselves are resilient. The applications built on top of them often aren’t.

Bank APIs time out inconsistently. Webhook delivery from financial institutions is unreliable — transactions arrive out of order, duplicated, or not at all. Reconciliation between what a bank’s API reports and what actually appears on a statement is a constant engineering problem.

Every fintech of any size in Nigeria has had to build its own reconciliation layer, its own webhook deduplication system, its own retry infrastructure. This is not a sign of a mature ecosystem. It’s a sign that the infrastructure layer hasn’t absorbed these reliability concerns so that application developers don’t have to.

The companies that get this right — Paystack’s webhook reliability, Flutterwave’s retry handling, Mono’s transaction normalization — are doing infrastructure work that, in a more mature market, would be solved at a lower layer.

Programmatic Credit Infrastructure

This is the most significant gap for the next phase of growth.

Credit scoring in Nigeria is still largely based on income verification and BVN-linked repayment history at formal institutions. The Credit Bureau system exists but coverage is limited. Most of the population and most small businesses operate with thin or no formal credit file.

The result: the teams building credit products are also building the infrastructure needed to make credit decisions — alternative data pipelines, account aggregation for cash flow analysis, repayment tracking. This is enormously expensive. It concentrates credit products in a small number of well-capitalized companies that can afford to build the infrastructure, instead of enabling a broader ecosystem of lenders.

What’s needed is a richer, more accessible credit infrastructure layer — one that makes cash flow data, repayment history, and alternative signals available programmatically. The components exist (Mono, Okra, Lendsqr infrastructure). The standardization and coverage needed to build at scale does not yet exist.

Multi-Currency and Cross-Border

For businesses operating across West Africa, cross-border payments remain a significant friction point.

PAPSS (the Pan-African Payment and Settlement System) is a meaningful development — it enables direct transactions between African currencies without routing through USD or EUR. But adoption is still limited, and the developer experience for integrating cross-border rails is significantly worse than domestic rails.

A Nigerian business trying to pay a Ghanaian supplier in cedis, or receive payments from a Kenyan customer in shillings, is navigating a fragmented set of integrations, compliance requirements, and settlement timelines. The engineering overhead is high enough that many businesses default to USD as an intermediary, which reintroduces FX risk and cost that regional rails were supposed to eliminate.

Enterprise Payment Infrastructure

The consumer payments story is largely solved. The enterprise payments story is not.

Large businesses — manufacturers, distributors, enterprise software companies — need payment infrastructure that integrates with ERP systems, supports complex approval workflows, handles bulk disbursements reliably, and produces reconciliation data in formats their finance teams can use.

Most of the payment APIs in the Nigerian ecosystem were designed for consumer and SME use cases. The enterprise requirements — audit trails, multi-signatory approval, real-time GL integration, bulk reconciliation at scale — are either not supported or require significant custom integration work.

This is the opportunity for the next wave of infrastructure companies: not another consumer neobank, but genuinely enterprise-grade payment infrastructure designed for the businesses that move significant volumes.

What the Next Phase Requires

The consumer fintech layer in Nigeria is crowded. There are dozens of neobanks, dozens of payment processors, and significant competition on every consumer use case.

The infrastructure layer is not crowded. The companies building reliable, developer-first financial infrastructure — not applications on top of that infrastructure — are fewer, and the opportunity is larger.

Developer experience. The quality of documentation, API design, SDK support, and developer relations at Nigerian financial infrastructure companies has improved significantly. It hasn’t reached the level where a developer can integrate a new payment rail in an afternoon. Getting there is a product and engineering investment, not just a regulatory one.

Reliability as a product. Uptime, webhook reliability, reconciliation accuracy — these need to be treated as features, not afterthoughts. The infrastructure companies that compete on reliability, not just on coverage, will win the enterprise segment.

Standardization across the credit data layer. The credit infrastructure gap is the most significant constraint on the next wave of financial products. Progress here requires coordination between bureaus, banks, and the CBN — but it also requires private-sector companies pushing the frontier on alternative data and sharing infrastructure costs.

Nigeria’s fintech infrastructure is strong enough to have built the products of the last decade. Whether it’s strong enough for the next decade depends on whether the ecosystem invests in the layer below the application — the reliability, the credit data, the developer experience, and the enterprise tooling that the most valuable financial products require.

Ellomas Technologies builds payment and operations infrastructure for businesses in Nigeria and across West Africa. We work across the fintech stack — from API integration to reconciliation systems to credit infrastructure.